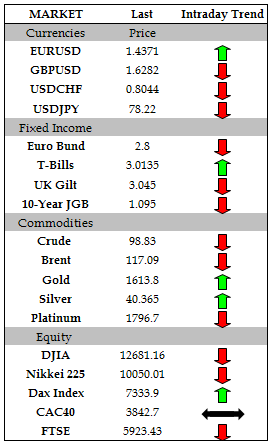

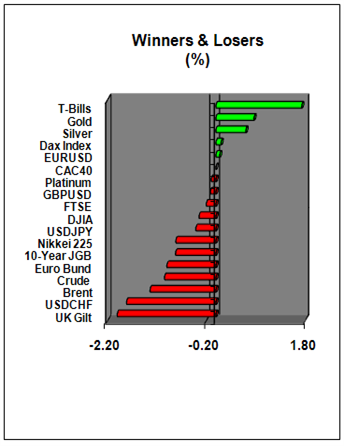

The U.S. dollar remained broadly lower against its major counterparts on Monday, as a lack of progress in talks aimed at raising the U.S. debt ceiling added to fears over a possible default, boosting safe haven demand.

During early U.S. trade, the greenback was fractionally higher against the euro, with EUR/USD dipping 0.03% to hit 1.4354.

Earlier Monday, ratings agency Moody's cut Greece’s sovereign debt rating by three notches to Ca, just one notch above default, after euro zone leaders last week agreed to another EUR109 billion in aid for the indebted nation, combined with EUR37 billion from the private sector.

The greenback was slightly higher against the pound, with GBP/USD slipping 0.13% to hit 1.6277.

Industry data released earlier showed that mortgage approvals in the U.K. rose slightly more-than-expected in June, as consumers pushed back expectations for a near-term interest rate hike by the Bank of England.

Elsewhere, the greenback was down against the yen and the Swiss franc, with USD/JPY shedding 0.19% to hit 78.39 and USD/CHF tumbling 1.54% to hit 0.8070.

In Japan, Finance Minister Yoshihiko Noda said earlier that recent currency moves were one-sided and that he was closely watching market developments.

In addition, the greenback was lower against its Canadian and New Zealand counterparts but dipped against its Australian cousin, with USD/CAD shedding 0.24% to hit 0.9455, NZD/USD inching up 0.02% to hit 0.8647 and AUD/USD sliding 0.12% to hit 1.0844.

New Zealand’s dollar remained supported close to its post-float high by expectations for a near-term interest rate hike by the Reserve Bank.

The dollar index, which tracks the performance of the greenback versus a basket of six other major currencies, was down 0.11%.

Fears over a possible U.S. default or sovereign downgrade escalated after talks between President Barack Obama and congressional leaders, aimed at raising the country’s USD14.3 trillion debt ceiling, broke down over the weekend.

Both Moody’s Investors Service and Standard & Poor’s have placed their credit ratings on U.S. debt on review for a potential downgrade.

Source : forexpros.com

Readmore...

During early U.S. trade, the greenback was fractionally higher against the euro, with EUR/USD dipping 0.03% to hit 1.4354.

Earlier Monday, ratings agency Moody's cut Greece’s sovereign debt rating by three notches to Ca, just one notch above default, after euro zone leaders last week agreed to another EUR109 billion in aid for the indebted nation, combined with EUR37 billion from the private sector.

The greenback was slightly higher against the pound, with GBP/USD slipping 0.13% to hit 1.6277.

Industry data released earlier showed that mortgage approvals in the U.K. rose slightly more-than-expected in June, as consumers pushed back expectations for a near-term interest rate hike by the Bank of England.

Elsewhere, the greenback was down against the yen and the Swiss franc, with USD/JPY shedding 0.19% to hit 78.39 and USD/CHF tumbling 1.54% to hit 0.8070.

In Japan, Finance Minister Yoshihiko Noda said earlier that recent currency moves were one-sided and that he was closely watching market developments.

In addition, the greenback was lower against its Canadian and New Zealand counterparts but dipped against its Australian cousin, with USD/CAD shedding 0.24% to hit 0.9455, NZD/USD inching up 0.02% to hit 0.8647 and AUD/USD sliding 0.12% to hit 1.0844.

New Zealand’s dollar remained supported close to its post-float high by expectations for a near-term interest rate hike by the Reserve Bank.

The dollar index, which tracks the performance of the greenback versus a basket of six other major currencies, was down 0.11%.

Fears over a possible U.S. default or sovereign downgrade escalated after talks between President Barack Obama and congressional leaders, aimed at raising the country’s USD14.3 trillion debt ceiling, broke down over the weekend.

Both Moody’s Investors Service and Standard & Poor’s have placed their credit ratings on U.S. debt on review for a potential downgrade.

Source : forexpros.com

This week was “a mixed blessing” for the euro. For the most part, the currency showed a good performance as worries about the debt crisis subsided, but by the end of the week concerns returned.

This week was “a mixed blessing” for the euro. For the most part, the currency showed a good performance as worries about the debt crisis subsided, but by the end of the week concerns returned.

Subscribe to email feed

Subscribe to email feed